Miners have applied for hundreds of permits across Colombia and Argentina in response to soaring demand for copper. A supply shortfall is predicted to occur by 2035, partly driven by the energy transition. Experts argue Latin America is well placed to capitalise.

Dialogue Earth, in collaboration with Climate Tracker, Mongabay and El Espectador, found that 201 mining licenses were active in Colombia, while a further 746 licence applications were still under review. Meanwhile, Argentina had 76 active copper mining licenses.

The UN Conference on Trade and Development characterises the energy transition as “fundamentally mineral-intensive”. Minerals such as copper are vital for a range of strategic developments, including solar panels, wind turbines, electric vehicles and electricity transmission grids.

But according to the International Energy Agency, the world could face a copper shortfall of around 30% by 2035 – the result of “limited resource discoveries and long lead times” for new projects.

This, says Ana Carolina González, director for Latin America at the Natural Resources Governance Institute, puts Latin America in an “interesting” position. Argentina and Colombia are pushing ahead with dozens of projects to accelerate extraction. José Cabello, a geologist with more than five decades of experience in Latin American mining, says geologists increasingly view Argentina, Colombia, Ecuador and Brazil as copper jurisdictions with high potential. Although they are not expected to surpass regional giants such as Chile and Peru in production, these countries are gaining prominence as globally relevant destinations for copper exploration and future supply growth, he adds.

Both the Colombian and Argentine governments have promoted their mining sectors as environmentally and socially responsible. Speaking in early July, Argentina’s newly appointed cabinet chief, Diego Santilli, emphasised the need for “responsible mining”; this concept has also been espoused provincially in the country. Colombia’s outgoing president, Gustavo Petro, for his part, has supported mining projects undertaken – as described by his government – in consultation with communities, and with environmental certifications.

While the region races to take advantage of copper demand, miners risk setting off on a collision course with communities.

Here, we present an analysis of satellite imagery showing proposed copper extraction sites in both countries. It reveals that many are in areas of environmental importance, or on community lands.

Chasing demand

In Colombia, the Mining and Energy Planning Unit (UPME) has highlighted the country’s geological potential for copper mining, “thanks to its diversity of geological formations, which manifest in different types of deposits and regions”. However, there is currently only one copper mine in operation. Another recently obtained the environmental permits to begin construction.

As for Argentina, Cabello says the discovery of deposits such as Taca Taca and Josemaría shows the country also has significant production potential. These are large-scale prospects that could rival northern Chile’s Chuquicamata, the world’s largest copper deposit. To date, however, the only active copper mine in Argentina – Martín Bronce in the north – achieves marginal production. According to the mining ministry, copper accounts for just 1.7% of Argentina’s total mineral exports.

Argentina’s Incentive Scheme for Major Investments (Rigi) seeks to bridge this gap by offering tax exemptions to developers of large projects. Twenty of the 36 submissions to Rigi over the past two years have been mining projects, according to the Rigi Observatory coalition of legal, academic and policy institutes. Five are copper developments, including Los Azules and one of Argentina’s largest mining investments in recent years, the Vicuña project.

The impact of mining projects on sensitive ecosystems

“We have been mining copper worldwide for many years, and this means that existing deposits are being depleted,” points out Ana Carolina González. Copper ore grades are also on the decline, having decreased in quality by 40% since 1991 according to the Australian mining giant BHP. “You need more and more land, over a wider area, to achieve the same quality as before,” she explains.

This expansion of the mining frontier will put more pressure on environmentally sensitive areas.

The Global Atlas of Environmental Justice, a database of environmental conflicts worldwide, shows that nearly a third of South America’s recorded conflicts are related to mining initiatives.

In Colombia, National Mining Agency (ANM) data shows that 37% of the country’s potential copper extraction sites overlap with “second-class forest reserves”, a category that restricts mining activities. “Excluded areas”, where mining is not permitted, covers 22%.

According to our analysis, however, there are at least 118 active licences for copper mining in the country that overlap with areas of environmental importance, such as forest reserves and protected areas. Of these, 24 are in areas currently considered “excludable” – where mining activity is supposed to be prohibited.

At least three active licences are in areas currently recognised and demarcated as páramos. This indicates ecosystems under protection because they regulate hydrological cycles supplying water to human populations. According to Colombia’s Ministry of Environment and Sustainable Development (MinAmbiente), páramos areas are key to the livelihoods of over 70% of Colombians.

Although their importance has been legally recognised since 1993, it was not until 2011 that MinAmbiente was mandated to demarcate them as off-limits to activities such as mining.

As for Argentina, data cross-referencing reveals that at least 21 mining projects are operating across five areas protected by international agreements, and national and provincial regulations.

One of the areas with the highest number of projects is the San Guillermo protected area, in the western province of San Juan. Designated a biosphere reserve by Unesco, five mining projects are currently operating in this national park. Two, the Josemaría and Filo del Sol deposits, are parts of the Vicuña project. They are operated by Lundin Mining and BHP respectively.

There are also 10 projects that overlap with or are located near glacial landforms, in areas defined by the Argentine Institute of Nivology, Glaciology and Environmental Sciences (Ianigla) as essential to glacial ecosystems. Most are in San Juan province, where there are 16 copper mining enterprises, including Los Azules, which is among the most progressed projects.

Leandro Gómez coordinates the Investments and Rights programme at Argentina’s Environment and Natural Resources Foundation (Farn), a coalition of lawyers who specialise in environmental law. He points to Argentina’s Glaciers Act, which prevented development close to glaciers but has been relaxed to promote mineral extraction.

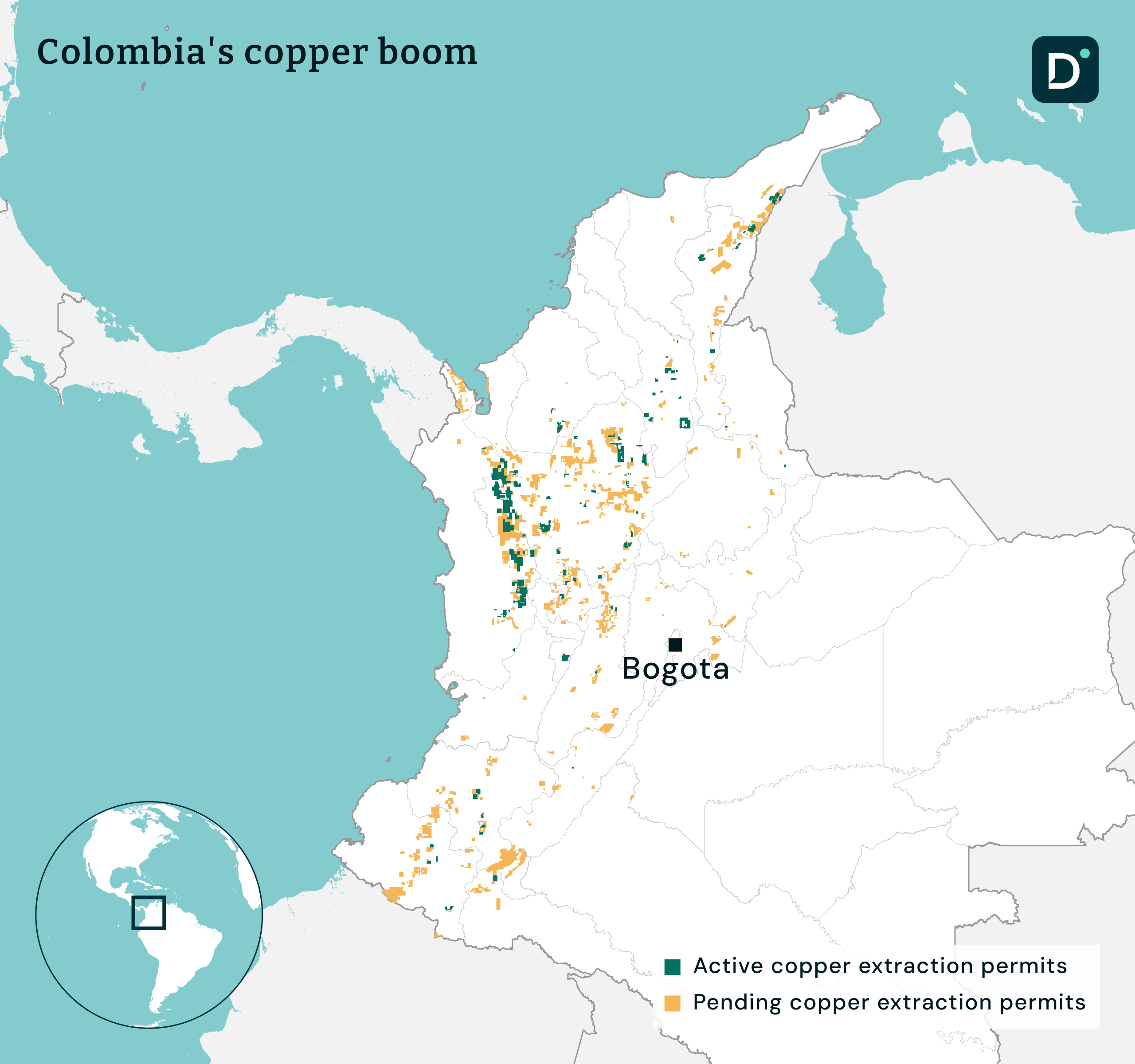

The copper map of Colombia and Argentina

Until mid-May, Colombia had only one copper mine in operation: El Roble, located in the municipality of El Carmen de Atrato, in Chocó, a north-western region renowned for its biodiversity. El Roble accounts for 85% of the country’s copper production, according to figures from the National Mining Agency. The remaining 15% is recovered gold mining byproduct.

In mid-May, the National Environmental Licensing Authority (ANLA) granted permission for the El Alacrán project, located in Puerto Libertador in the northern region of Córdoba. This was the final permit needed to begin construction. According to the project’s feasibility study, the site contains a “probable” 98 million tonnes of mineral reserves that include copper, gold and silver. The company running the project, CMH Colombia, claims the mine is projected to process 17,000-20,000 tonnes of ore per day – around 20 times the processing capacity of Colombia’s only active copper mine, El Roble.

There are hundreds of other projects at various stages across Colombia. Analysis of public records reveals at least 210 active medium- and large-scale mining licences nationwide that involve copper. Most are in the departments of Antioquia (77), Chocó (51), Bolívar (22), La Guajira (14) and Córdoba (11).

Of these 210, according to data from the mining register, one is at the preliminary technical assessment stage, 89 are at the exploration stage, 17 are in the construction and commissioning phase, and 103 are in production.

Interest in new Colombian copper projects has accelerated significantly over the past decade. According to our analysis, nearly 332 applications were filed in 2021 and 2022 alone. Currently, there are at least 746 active applications under assessment by the mining authority that target copper to some degree: 673 medium-scale, 73 large. Copper is the primary target for 80 projects.

In Argentina, copper prospecting is concentrated around the Andes – there are at least 77 projects in the area. Of these, 68 are in the exploratory or pre-exploratory phase, eight have progressed beyond exploration and one is in production. Most of the projects are in the provinces of Salta (46) and San Juan (16). The others are in La Rioja (6), Catamarca (4), Mendoza (2), Neuquén (1) and Río Negro (1).

Mining projects and community lands

The Colombian constitution does not prevent mining in Indigenous reserves or communal lands, but it does require local communities to be consulted. Our analysis reveals that at least 94 mining licences involving copper overlap with Indigenous reserves (64), community councils of Afro-descendant communities (54) and two zonas de reserva campesina (zones demarcated for peasant farmers).

Concessions covering more than 69,000 hectares have been awarded within 30 Indigenous reserves. Most of them (77%) are situated on the lands of the Embera people. There are at least 18 mining concessions on Afro-descendant community council territories. Most of the licences on these territories (26 out of 54) were applied for by the company Exploraciones Chocó Colombia.

In Argentina, the provinces where copper projects are located are home to more than 110 communities belonging to a range of Indigenous peoples. The country has recognised Indigenous lands since 1994, but they are still not clearly defined.

Of the 76 mining projects listed by Argentina’s Secretariat of Mining, 47 are less than 50 km from Indigenous territories; 17 within 15 km, and three – all in the province of Salta – are less than 4 km away. According to official data, communities of the Calchaquí and Tastileas peoples live in these areas.

The scope of this investigation did not include determining whether Indigenous communities have been adequately consulted in each of these cases. However, the importance of the work that Indigenous peoples do to protect crucial environments is widely recognised – as are the battles against extraction and development that these communities are forced to fight, including in Argentina and Colombia.

In the sights of the major powers

China, the US and the European Union have all sought to strengthen their presence and forge new alliances in mineral-rich Latin America.

Chinese companies have invested in numerous projects, and between 2013 and 2024, China’s President Xi visited Latin America six times. China’s most recent policy document on Latin America and the Caribbean indicates a desire to “strengthen cooperation” on issues relating to clean energy and “enhance green development and utilization of mineral resources”.

If countries, as a bloc, fail to agree on maintainingAna Carolina González, Latin America director, Natural Resources Governance Institute

these minimum standards, what has been termed a

‘race to the bottom’ could begin

China’s interest is not new, notes David Castrillón-Kerrigan, who researches the impacts of Chinese foreign policy in Latin America at the Externado University of Colombia: “Previously, demand was driven by other needs, such as infrastructure development. But now, China’s economic structure has changed and it produces different kinds of goods, with added value.” The rapid development of the Chinese electric vehicle industry, for example, has driven demand for critical minerals.

Meanwhile, in 2025 the European Union said its demand for copper could increase by more than 50% by 2050. The bloc has emphasised that Latin America and the Caribbean is “more strategically important than ever” for securing a supply of transition materials.

In the US, President Donald Trump has also set his sights on transition materials. In January, he ordered officials to conclude bilateral agreements with allies to secure supplies of copper and other metals. This is with the aim of not being “dependent on imports from foreign adversaries”.

González says Latin America has made progress on regulatory frameworks, setting minimum standards on social, environmental and governance issues. But in times of political instability these could be put at risk: “If countries, as a bloc, fail to agree on maintaining these minimum standards, what has been termed a ‘race to the bottom’ could begin.” This could lead to regulations being relaxed to attract investment, she warns.

González adds that countries should take a firm stance on upholding these minimum standards, and demand projects generate added value and contribute to local development. They must also ask where the demand is coming from: “We know that this demand stems from energy issues, but it is also linked to artificial intelligence and military applications. If we continue to demand minerals at this level, no ecosystem will be able to cope.”

This article was produced with the support of Climate Tracker Latin America. The data analysis was based on medium- and large-scale projects applied for by companies, legal entities or associations, with a cut-off date of 15 May 2026, the date on which the information from the mining register was accessed.