The International Energy Agency (IEA) has just released a special report on India’s energy outlook that maps out both the constraints and challenges that the country faces. According to the IEA, India is already the single largest contributor – about 25% – to growth in energy demand globally. As India hosts 18% of the global population, and accounts for only 6% of global energy use, the IEA estimates that the growth in demand will continue.

It bases its assumption on three crucial factors:

1) one fifth of the Indian population – 240 million people – still do not have access to electricity and two-thirds do not have access to clean cooking fuel;

2) India is rapidly urbanising, driving up energy demand; and

3) the Indian government has committed itself to expand manufacturing growth through initiatives such as the “Make in India” campaign, which will require massive growth in energy supplies to be successful.

The irreducible cost of oil

The report, focusing on growth until 2040, estimated that the European Union, US and Japan would see negative growth in energy demand as the populations aged, and energy use was cut back. Growth was predicted in Latin America, the Middle East and Africa, with China’s demands growing faster still. India would still be the leader in energy growth, much of it carbon based. Dr Fatih Birol, the IEA Executive Director, said that the IEA estimated that by 2040 India will triple coal production while also increasing imports.

India will also become the largest oil importer in the world, with 63% of it coming from the Middle East. The IEA highlighted the costs of oil imports to the Indian economy, stating that, “India’s growing reliance on oil and gas imports carries with it a large bill. The value of India’s net oil and gas imports grows from USD 110 billion in 2014 to more than USD 300 billion in 2030 and USD 480 billion in 2040 (of which gas accounts for some 10-15%). This represents a sizeable share of India’s overall GDP – 5.3% in 2014 and 4.6% in 2040.”

The promise of renewables

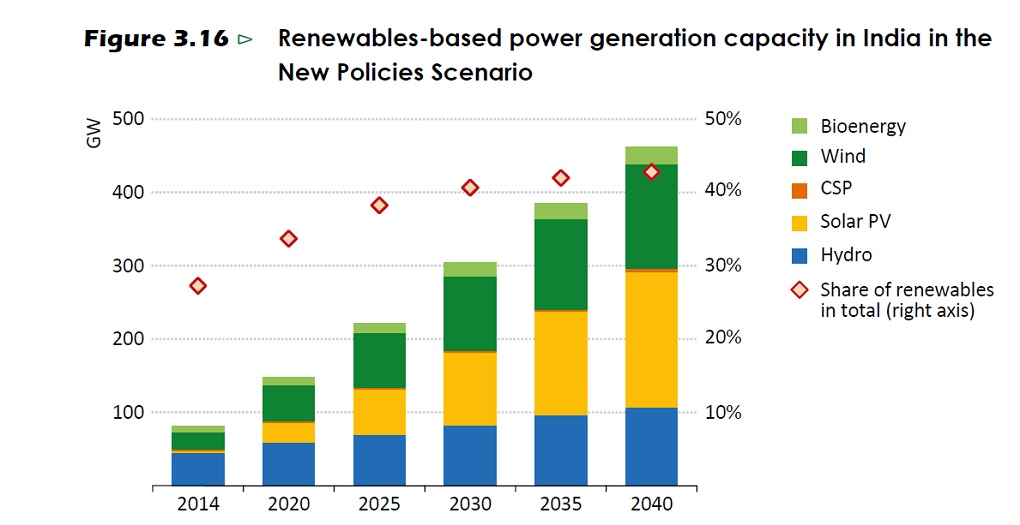

The great bright spot was the expansion of renewable energy. The IEA envisages a massive expansion of installed capacity based on renewable energy, going from less than 100 GW in 2014, to more than 450 GW in 2040.

The IEA projections clash slightly with those of India in its Intended Nationally Determined Contribution (INDC), as the IEA projects that India will only be able to build an installed capacity of 150 GW from renewables by 2020, which makes it difficult to believe that India would achieve a 175 GW installed capacity by 2022 as it has promised in its INDC. Nevertheless by 2030, the IEA estimates that India will derive more than 40% of its energy through renewable energy, exactly in line with the INDC.

Clouds of pollution

Nevertheless one of the key sources of energy will be coal, either just a little less than renewables or a little more, as one of the two biggest sources of energy. This, as well as the massive growth, will have a major effect on air pollution. The outcomes are fairly scary, with the IEA stating:

“The rise in outdoor PM2.5 emissions alone is calculated to lead to a reduction in life expectancy of more than seven months (this is in addition to the 16.8 months in reduced life expectancy that is a result of current PM2.5 levels). This corresponds to a 140% increase in premature deaths, which reach 1.7 million in 2040. Indoor air pollution, from the continued though diminished use of solid biomass for cooking, could be expected to add considerably to this number. In addition, the rise in ground-level ozone leads to crop losses. By 2040, the increase in ground-level ozone gases leads to a 13% decrease in wheat yield and will have adverse impacts additionally on soybean, rice and maize crops.”

Strict policies to control and deal with the levels of pollution will be a must. Additionally water usage by coal plants – which account for 95% of water usage in the energy sector – as well as the effects of climate change, threaten to add a dark lining to India’s bright energy future.

Lastly the IEA estimates that India will need an annual investment of more than USD 100 billion from 2015-2040 to make this great transition, a challenge indeed, since between 2005-2014, the investment level has been just over USD 60 billion per annum.