Across Southeast Asia, governments continue to view coal as a reliable and inexpensive energy source, despite the rapidly falling costs of renewable power and the growing number of companies making vocal commitments to meeting all their demand with it. These companies are clear about what governments need to do to help them maintain and grow their businesses: no more coal in national energy grids, better support for renewables, and long-term strategy on fields such as electric transport, energy efficiency and ecosystem protection.

H&M Group has been at the forefront of these calls in Cambodia, working closely with leading companies across industry and Cambodian government ministries, among others. We want to ensure that fossil-free energy production is at the centre of discussions around future business growth.

Cambodia is a major producer of garments, footwear and, increasingly, bicycles, with over 800,000 people working in the garment sector from a population of about 15 million. However, power shortages in the 2019 dry season exposed the weaknesses of the country’s grid, which relies heavily on hydropower. The shortages impacted industrial production and necessitated the use of expensive diesel generators for substitute power. The government’s response was to approve a spate of heavy oil and coal projects that lack transparency on financing and pricing, as well as published environmental impact assessments. These short-term actions to boost installed capacity show that the government is willing to ignore both the environmental risks and the emerging industry consensus on the need to phase out high-carbon energy sources, at a time when most countries are doing exactly that.

Brand reputation at risk

While renewable energy construction is growing across the region, coal power still plays a worrying role in many national energy plans. This will have long-term impacts for energy pricing and for how companies judge where to source their products. For example, a 100 megawatt on-site coal power plant under construction at Cambodia’s Sihanoukville Special Economic Zone, which was intended to provide a more constant power supply, now means no brands that have made commitments to reduce their carbon footprint will find the zone attractive – why pay to offset the carbon of a 100% coal-powered factory when low-carbon alternatives exist elsewhere?

Why pay to offset the carbon of a 100% coal-powered factory when low-carbon alternatives exist elsewhere?

And these are the decisions that companies will increasingly make as they look beyond labour costs, energy costs and suitable infrastructure when deciding where to invest or work. Under the RE100 project, companies have committed to using 100% renewable energy by a particular date, which, in the case of H&M Group, is 2030. Companies are also getting onboard with the Science Based Target initiative (SBTi) – a public commitment to make energy decisions that reduce global warming.

If Cambodia is to continue to be a competitive destination for foreign direct investment, it is vitally important that the country’s energy grid remains as fossil-free as possible. Other countries that are competing to attract the same investment and employment are already making moves in that direction. Myanmar recently tendered 1 gigawatt of solar projects, Vietnam is cancelling/postponing 50% of planned coal projects and Bangladesh is revaluating 90% of its planned coal projects. Meanwhile, Cambodia has already become a destination for outdated and polluting coal technology and has more than 4 gigawatts of coal projects in construction or planned over the next few years.

Time to pivot

Cambodia is in the enviable position of having a reasonably green grid, which in 2020 comprised some 50% renewable energy, mostly hydroelectric. Neighbouring Vietnam boasts less than 10% renewables, while Sweden, where H&M Group is from, had more than 55% in 2019. But the current pipeline of planned energy projects would see Cambodia reduce its share of renewables on the grid to only 26% by 2030. Such a move would throw away Cambodia’s advantage over neighbouring countries. It would also leave the country more exposed to other climate policy measures defined elsewhere such as the carbon border tax being considered in Europe.

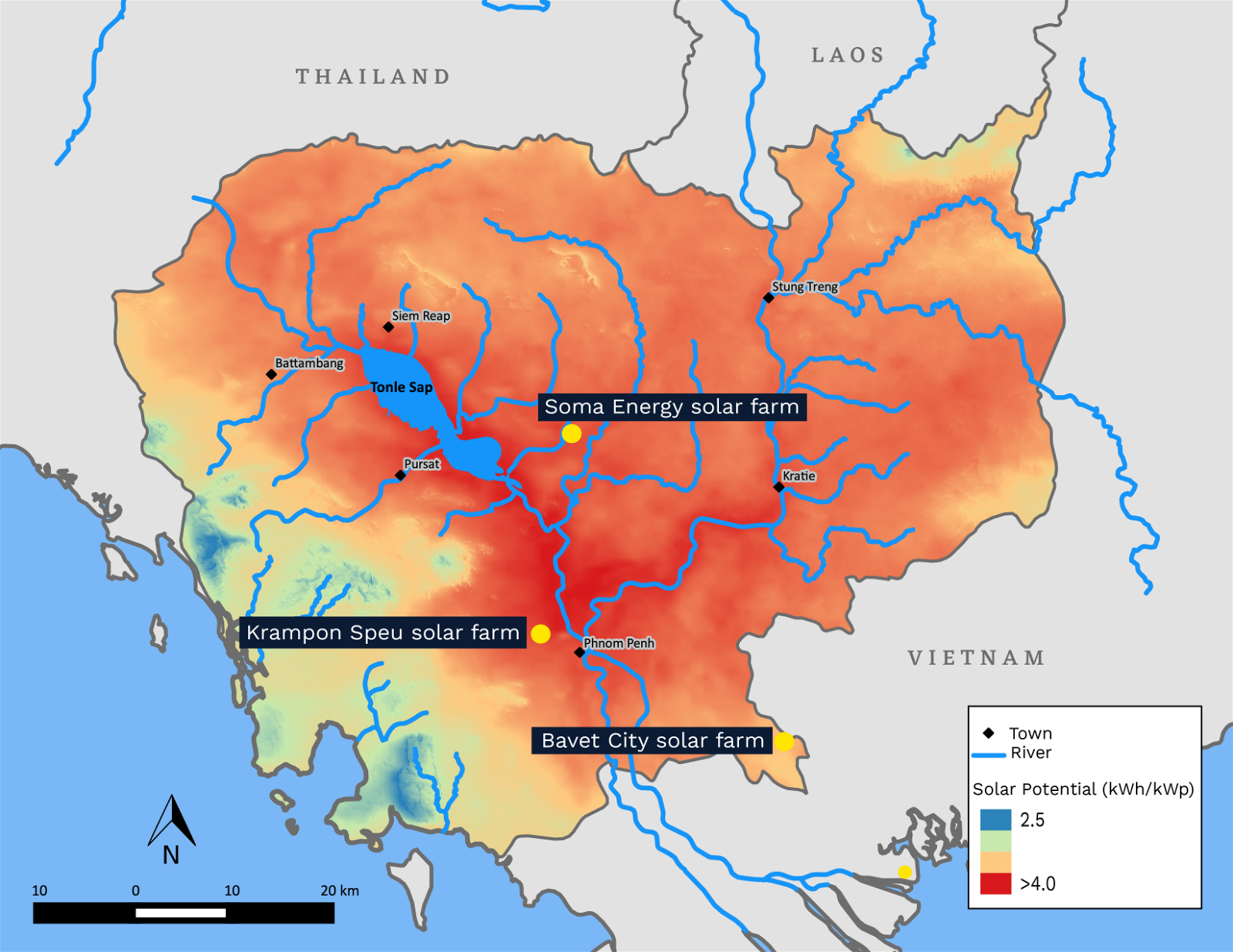

Cambodia’s energy landscape has transformed in the past few years and whilst hydroelectric and coal dominate, solar is also seeing some growth, with 200 megawatts of installed capacity expected by 2021, from zero in 2018.

While energy reliability and price are important, industry commitments to carbon neutrality eclipse all other energy requirements

With the right policies to expand renewables, Cambodia could leverage its low-fossil grid to not only keep those brands that are already invested in the country, but attract new ones committed to becoming carbon neutral. While energy reliability and price are of course important, industry commitments to carbon neutrality eclipse all other energy requirements, both for brands and consumers.

Carbon reduction commitments by companies are real, and actions to meet them have been underway for some time, driven by consumer demand, a growing understanding in industry of environmental impacts across supply chains, and how such commitments can be utilised to focus and drive internal product development and planning.

Cambodia’s solar potential

While RE100 or the SBTi targets are not legally binding, consumer attention and focus is such that it would be near impossible to walk back from them now; consumers were demanding greener and cleaner products before Covid-19, and that has only strengthened subsequently.

Energy efficiency, rooftop solar and the cleanest grid possible are all needed to ensure that carbon offset credits – the final step for 100% renewable energy production – is as affordable as possible. The dirtier a national grid, the more carbon offset credits will be needed to achieve “zero”.

Labour and logistics costs, plus production times and quality will continued to be important. But, simply put, the location of orders will change if the price of neutralising carbon is higher in one sourcing country than in others due to the value of carbon credits needed.

It is therefore imperative for export-focused countries such as Cambodia to pause current coal plans and re-evaluate how industrial requirements for cleaner energy will be met.

The future is clear: grid energy must get cleaner, and investors and industry will find more attractive countries that are able to offer such energy opportunities.