Compounded by the Covid-19 pandemic, a number of richly biodiverse countries in Latin America face converging fiscal and environmental crises, increasing competition for the resources needed for conservation and climate action.

On the opening day of COP26 climate talks in Glasgow, Ecuador’s president Guillermo Lasso announced a new 60,000 square-kilometre marine protected area (MPA) around the mega-biodiverse Galápagos Islands. The new MPA would place limits on industrial fishing and create a living scientific laboratory for the benefit of the world, he said, adding that it will be founded through a debt-for-nature swap.

The presidents of Argentina and Colombia – two heavily indebted countries that the UN’s Convention on Biological Diversity (CBD) ranks among the most biodiverse in the world – have also called for debt-for-nature and debt-for-climate swaps as possible solutions.

So what are they and how do they work?

The idea behind debt-for-nature swaps

In 1984, as Latin America experienced a profound debt crisis, Thomas Lovejoy, a former scientist at the World Wildlife Fund (WWF, now known as the World Wide Fund for Nature), wrote an article for The New York Times titled “Aid Debtor Nations’ Ecology”, regarded as the intellectual birthplace of debt-for-nature swaps.

As debtor nations cut government spending, programmes for protecting natural resources are usually among the first to go, Lovejoy observed. He feared the consequences for ecosystems of cuts to Costa Rica’s national park budget or Brazil’s environmental protection agencies – examples that still resonate powerfully today.

“Why not use the debt crisis – which seems to be nearing financial gridlock – to help solve environmental problems?” Lovejoy asked, arguing that if debtor nations committed to protecting natural resources, then they could be made eligible for discounted debt.

The benefits would be felt long after the debt problem is solved. Swap initiatives would not need new injections of hard currency, and would boost the debtor country’s ability to repay loans. Conservation projects would also be paid for in local currency, so resources would go further than they might in servicing debt.

As well as increasing the likelihood of being repaid, creditors might even get “a measure of satisfaction”, Lovejoy suggested.

How do debt-for-nature swaps work?

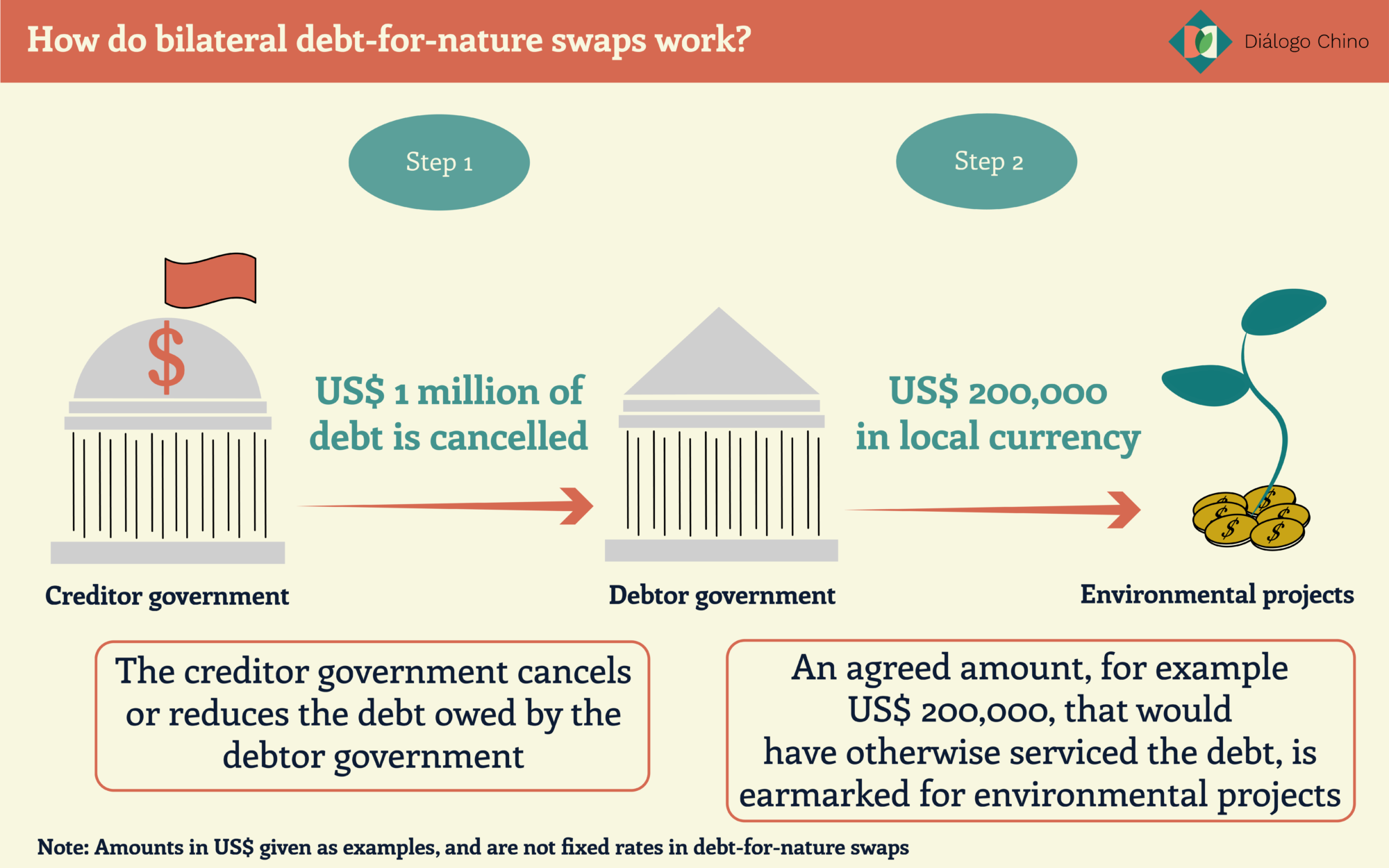

Debt-for-nature swaps are typically a voluntary transaction in which an amount of debt owed by a developing country government is cancelled or reduced by a creditor, in exchange for the debtor making financial commitments to conservation.

Swaps typically involve countries that are financially distressed and experiencing difficulties in repaying foreign debts. The earnings generated through swaps are often administered by local conservation or environmental trust funds.

Creditors could be developed country governments, commercial banks or even private companies. Commercial debt swaps involve selling a commercial bank’s debt on secondary markets at discounted rates. Bilateral debt swaps involve government debt, known as sovereign debt, and typically require a restructuring plan for the debtor country.

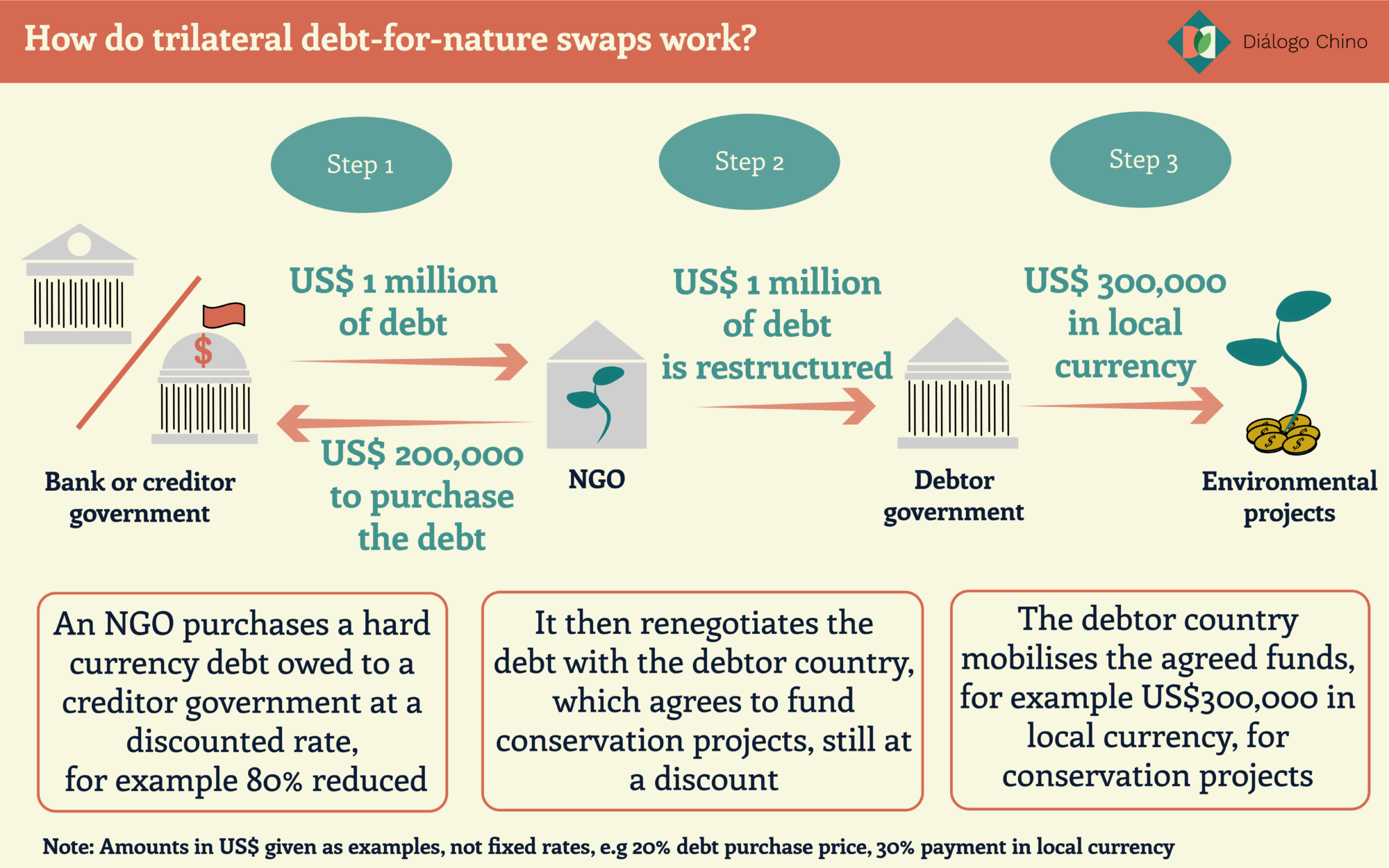

There are also ‘trilateral’ swaps. For these, an NGO purchases outstanding debt from the creditor on a secondary market at discounted rates, and then renegotiates the debt obligation with the debtor country. The NGO then sells the debt back to the debtor at a lower price.

When the debtor repurchases its debt, the obligation is forgiven. A portion of the capital that would have otherwise gone to paying off the original commitment is channelled towards grants, bonds or funds for pre-agreed investments in conservation programmes or the implementation of environmental policies.

Latin America and the first debt-for-nature swap

In the 1970s and early 1980s, which became known as Latin America’s “lost decade” of development, many of the region’s governments took out sizeable loans from commercial banks or foreign governments. There was a growing concern that much of the debt would never be fully repaid and, therefore, its value was lower.

When Mexico defaulted on its US$80 billion foreign debt in 1982, many other debt-distressed Latin American countries followed suit, confirming creditors’ fears.

In 1987, the environmental NGO Conservation International arranged the world’s first debt-for-nature swap, between Bolivia and foreign creditors, who forgave US$650,000 of its debt, a portion of the total. In exchange, the Bolivian government agreed to set aside 3.7 million acres of land adjacent to the Amazon Basin for conservation.

A number of other Latin American countries participated in debt-for-nature schemes in the 1990s. Notable among them are Belize and Costa Rica, the two countries that, as of 2003, had generated the most conservation funds as a share of their total debt treated – 108% and 68%, respectively – according to the Organisation of Economic Cooperation and Development (OECD).

The Nature Conservancy and WWF, among other NGOs, have also been intermediaries in trilateral debt-for-nature swaps in Latin America and the Caribbean.

Why are they relevant now?

While debt-for-nature swaps have waned in popularity since the 1990s, they are still employed in innovative ways across the world. In 2018, the Seychelles collaborated with the UN and the Nature Conservancy to forgive US$21.6 million of its debt. It was the first debt swap of its kind to focus on the conservation of a marine ecosystem.

Amid the economic fallout from the pandemic, Latin American countries are failing to allocate the resources they have to long-term sustainability, as well as mitigating and adapting to the effects of climate change.

In 2020, the 33 countries of the region allocated US$318 billion to fiscal and stimulus measures in response to the Covid-19 pandemic, of which $46 billion went to recovery spending. Just US$1.47 billion of that qualifies as ‘green’, according to research by the UN and Oxford University. At a mere 0.5%, the percentage of environmentally sustainable spending is significantly lower than the 19.2% it calculates as the global average.

Today, countries with pressing fiscal problems that may have been exacerbated by the Covid-19 pandemic, such as Argentina, Colombia and Ecuador, face a conundrum. Their biodiversity is under threat from the expansion of the agriculture and extractive industries they rely on for export revenues to service their debt.

Without funds to protect ecosystems, their long-term integrity and the services they provide for the wider economy, such as carbon sequestration and water, could be compromised.

“Traditionally, debt-for-nature swaps have usually involved creating new protected areas in relatively intact or threatened habitats,” according to Blake Alexander Simmons, a conservation scientist at Boston University’s Global Development Policy Center. He added that although contemporary debt swaps are getting more creative, new protected areas remain one of the comparatively easier actions to implement.

But they aren’t always the best solution.

“Protected areas may not be the most effective or equitable solution to conservation issues, and there may be more urgent threats in landscapes that are not intact, like pastoral or agricultural lands,” Simmons said.

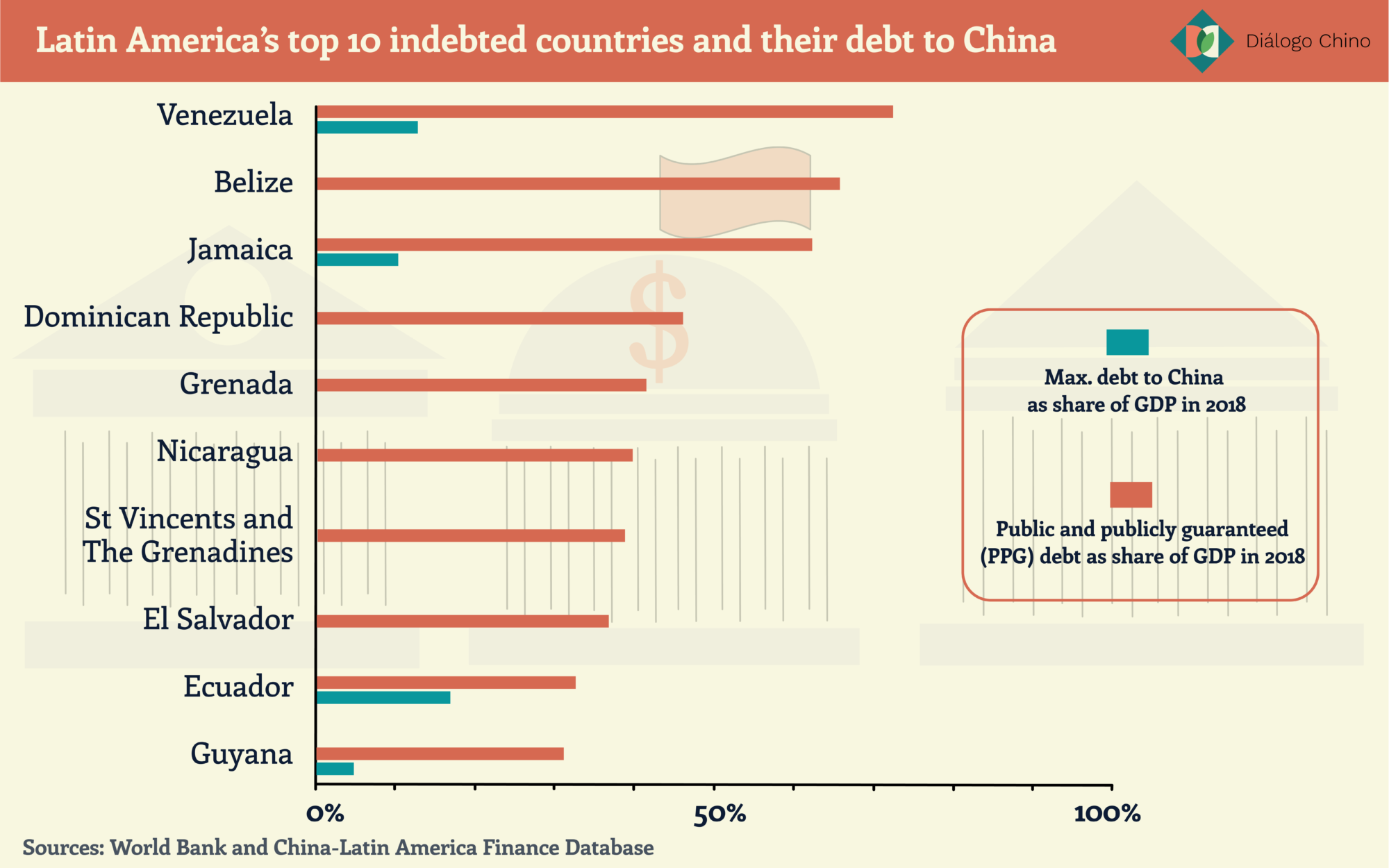

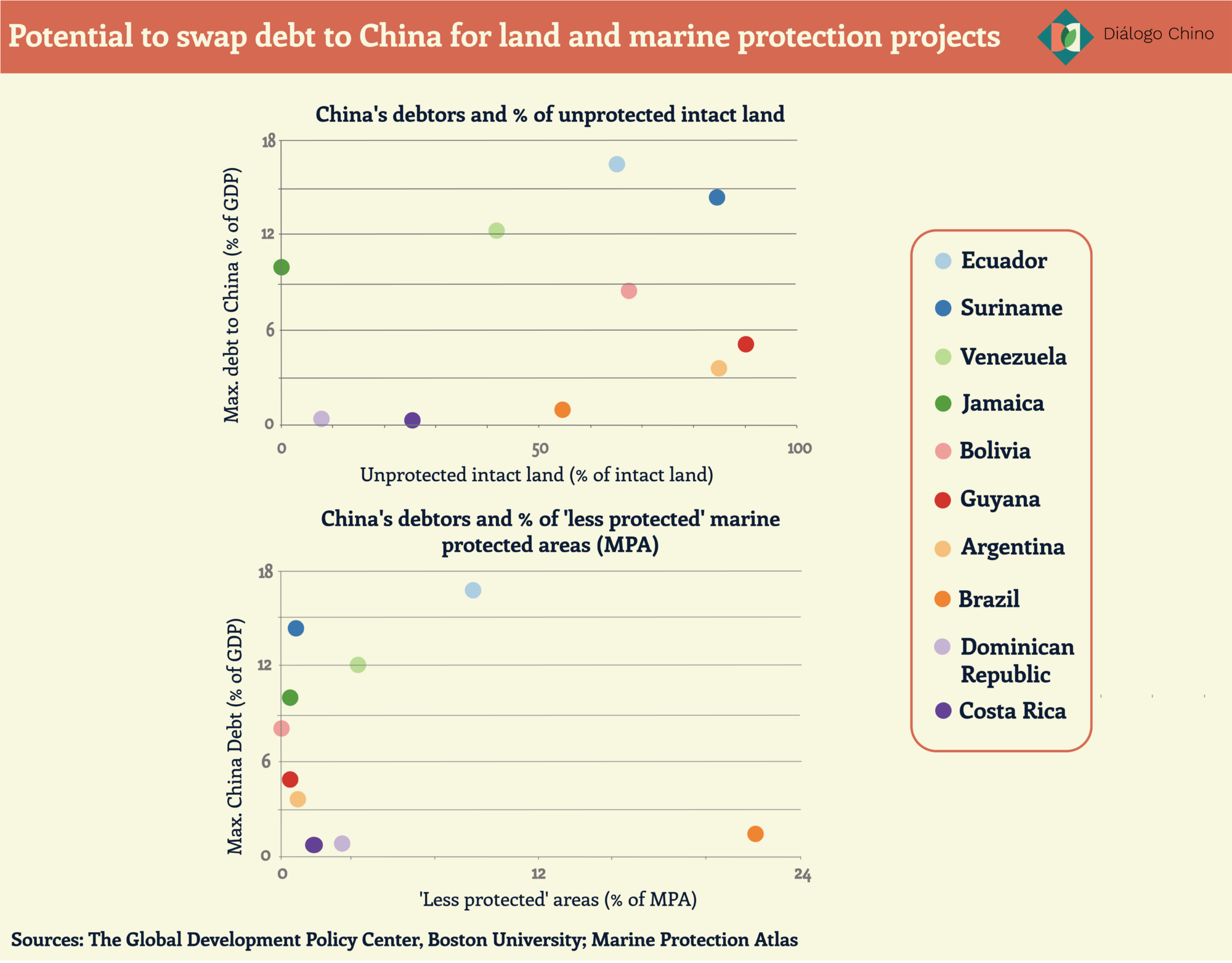

Boston University recently published an interactive map that assessed the opportunities for China, the world’s largest bilateral creditor, to engage in debt-for-nature swaps worldwide. Venezuela, Ecuador, Jamaica and Guyana all have comparatively high levels of debt to China as a share of their GDP and in relation to their overall public debt (as of 2018).

Their data compares a country’s estimated amount of bilateral debt to China (the official figures often aren’t disclosed) and the area of unprotected intact land that could be conserved.

These metrics, the researchers argued, help build up a picture of how China and its debtors could pursue mutual environmental goals through debt relief. Though few countries are currently listed as having high potential for debt-for-nature swaps with China in particular, the researchers identify Ecuador, which owes an estimated US$18 billion to China, around 17% of its GDP, as having “moderately high” potential for a debt swap in exchange for climate action. “Debt-for-climate swaps” are an adjacent concept, in which debt is exchanged for investment into climate projects, though these aren’t necessarily nature-focused.

What are the disadvantages?

Despite the general view that debt-for-nature swaps are mechanisms that can achieve positive environmental policy outcomes, they have yet to achieve widespread approval. International organisations have raised concerns over the perceived inefficiency and risks of swaps compared to other financial instruments.

The UN released a report in 2017 reviewing the practice and evaluating their benefits and risks. While it found that swaps could improve a country’s credit standing and grant its government access to financial services for economic and social development, the risks and inefficiencies associated with poorly implemented swap deals can be significant.

Debt-for-nature swaps can also take years to negotiate, which can be expensive. Particularly time-consuming are the negotiations between debtor and creditor countries over the scope of conservation measures. Delays increase the cost of operations, and even after a painstaking process, negotiations may never come to a satisfying conclusion.

Following Bolivia’s 1987 swap deal, NGOs and US policymakers turned their attention to a similar deal with Brazil in 1989. Despite advanced negotiations for up to US$8 billion of Brazil’s foreign debt to be forgiven, the country’s leaders opted at the last minute to close-off the Amazon from any direct financial aid from foreign governments.

Debt-for-nature swaps might, however, be about to make a return to the table for Latin American countries, with Argentina’s president Alberto Fernández recently calling for swaps as a way to address a growing debt crisis. The upcoming COP26 summit and, particularly, the second segment of the COP15 biodiversity talks in 2022 may also see debt-for-nature swaps climb higher on the agenda.