![<p>While Chinese private investment overseas has largely been in renewables, state owned enterprises overwhelmingly invest in fossil fuel industries [image courtesy: WRI]</p>](https://dialogue.earth/content/uploads/2018/11/ThinkstockPhotos-854613344-768x512.jpg)

The world is running out of time to take action and limit the worst impacts of climate change. The IPCC has issued stark warnings that we have to cut carbon pollution by half by 2030 and wean our global economy completely off carbon by 2050.

Meanwhile China’s Belt and Road Initiative (BRI) promises to plough USD 1 trillion into energy and infrastructure across over 100 countries. It will play a determining role in shaping the direction of future development, particularly among emerging economies – and whether we meet our climate goals.

Launched by President Xi Jinping in 2013, BRI encompasses land routes (the “Belt”) and maritime routes (the “Road”) with the goal of improving connectivity in the region primarily through infrastructure investments. BRI has become a wide umbrella term for China’s foreign policy – its vision of a future world and its place within it.

A new report by the World Resources Institute (WRI) – “Moving the Green Belt and Road Initiative: From Words to Actions” – remains upbeat. There is a huge opportunity for Chinese investment to support green low carbon development in BRI countries, if it is channelled in the right way, the authors argue. But there is a danger Chinese investment locks countries into fossil fuel intensive polluting development model for decades to come.

Green rhetoric

Chinese officials claim the Belt and Road Initiative will be ambitious and green. The Ministry of Environmental Protection (now the Ministry of Ecology and Environment) has released Guidance on Promoting Green Belt and Road, and the Belt and Road Ecological and Environmental Cooperation Plan. However these documents are conceptual, rather than offering concrete rules for Chinese banks and companies investing overseas.

In reality, Chinese overseas investment is still flowing into China’s old development model – into fossil fuel intensive polluting projects, as new findings from WRI show.

WRI teamed up with Boston University’s Global Development Policy Center to analyse Chinese energy and transportation investments between 2014-17 in 31 BRI countries and assessed whether they aligned with countries’ national climate plans, or “Nationally Determined Contributions (NDCs)“, submitted as part of the international Paris Agreement on climate change.

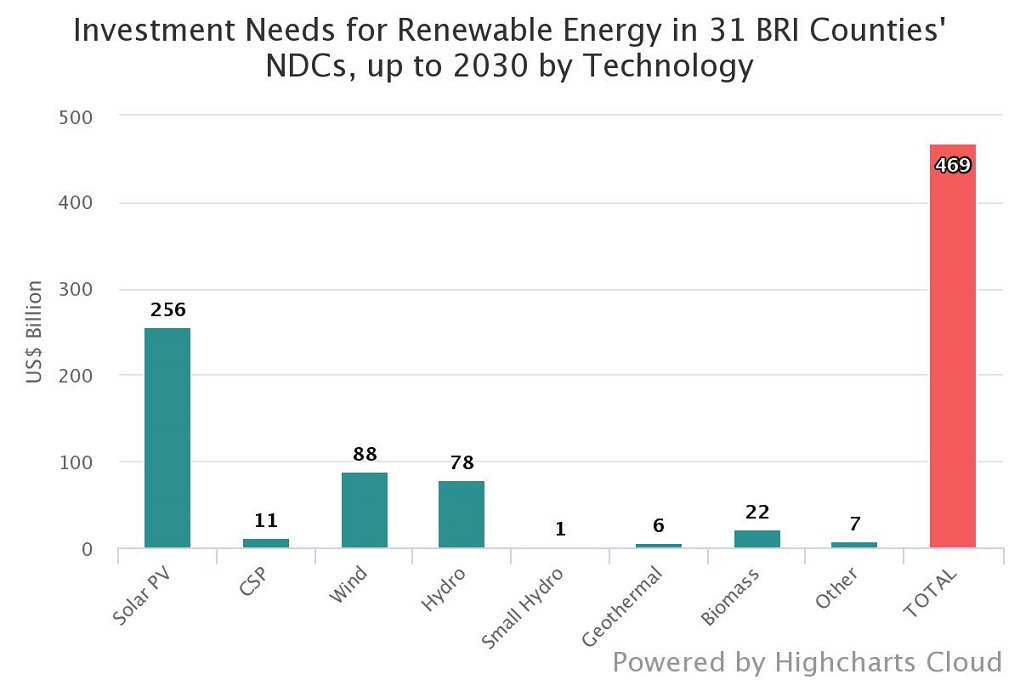

The research teams found enormous opportunities for green investment in national plans. Those 31 countries alone will need about USD 470 billion just to implement renewable energy commitments.

However, most Chinese deals in energy and transportation are still tied to carbon intensive sectors and do not align with low-carbon priorities included in BRI governments’ NDCs.

Some key findings from the report:

- Between 2014 and 2017, six Chinese banks – the China Development Bank (CDB), the Export-Import Bank of China and the “Big Four” state-owned commercial banks – participated in USD 143 billion worth of syndicated loans to the BRI region’s energy and transportation sectors. Almost three-quarters of the total volume of this finance went to the oil, gas and petrochemical industries. Of the finance that went to the power-generation sector, more than half financed fossil fuel power plants, including USD 10 billion for the coal plants.

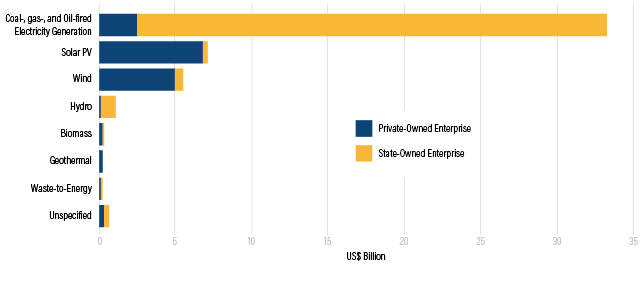

- Over the same period, 93% of energy-sector investments by the state owned Silk Road Fund were also in fossil fuels, and 95% of cross-border energy investments by Chinese state-owned enterprises (SOEs) were in fossil fuels as well.

- In contrast, nearly two-thirds (64%) of cross-border energy-sector investment by Chinese privately owned enterprises were in renewable energy.

- While SOEs invested less than USD 1 billion in solar PV and wind over the same period private enterprises invested heavily in solar PV and wind power, reaching USD 7 billion and USD 5.5 billion, respectively, over the four-year period, with India and Pakistan being the top investment destinations.

- In the transportation sector, the majority of Chinese deals were in traditional transportation, such as aircraft financing, airports, road construction, and car manufacturing, rather than lower-carbon options, such as urban public transit and railways.

The report argues China could become a major catalyst for low carbon development in the region: “If Chinese government special funds are deployed to give greater priority to green opportunities, especially in the near term, these funds could have an outsized positive impact on green growth in the BRI countries”. …Moreover, such initial investment would help encourage countries to ramp up their climate ambitions and revise their NDCs under the Paris agreement after 2020.

Multilateral Development Banks (MDBs) have adopted targets aiming for over 25% of their overall portfolio to go towards climate finance, the report points out. “If special funds allocated for BRI were similarly deployed, this would channel more than $28 billion additional dollars in support of climate finance and NDC priorities at a critical time for BRI countries.”

No oversight, no regulation

The gap between rhetoric and reality highlights the major problem: there is no system of oversight to ensure Chinese overseas investment flows into the right kind of projects.

The government has drawn up green guidelines for overseas investment, but these are voluntary, have no teeth and are rarely if ever enforced. There are no overarching guidelines for the sustainability requirements of Belt and Road projects beyond individual institutions. Though a group of Chinese and foreign NGOs have committed to helping China develop such guidelines under the umbrella of the China Green Leadership: Belt and Road Green Development project.

Moreover, BRI was in part designed to absorb China’s overcapacity in the coal, steel and cement production to boost the domestic economy and help clean up the environment at home. So far this looks set to perpetuate a carbon and pollution economic intensive model elsewhere. And so as China closes coal-fired power stations at home, it supports the construction of new coal power stations in Pakistan, Vietnam, Indonesia and elsewhere. Its policy banks build oil pipelines across Myanmar and Russia, and its state-owned companies set up cement and steel factories in Central and Southeast Asia.

At the same time, China is positioning itself as a global green leader. It is emerging as a powerbroker in global climate talks ahead of the next UN meeting filling in the vacuum left by US president Donald Trump and hosting the preparatory meetings that will set the tone for the COP24 summit in Katowice, Poland, in December.

They key question is then whether China “will help deliver a strong set of rules of the Paris agreement and redirect finance away from coal,” as Laurence Tubiana, chief executive of the European Climate Foundation think-tank and one of the architects of the Paris accord recently told the Financial Times.

Under the Paris accord, more than 190 nations pledged to work together to limit global warming to well below 2C, but it is up to each country to set its own targets for how to achieve that.

In Poland, countries will decide how to implement these commitments, and how to significant ratchet up the ambition of current goals in the coming years, which is essential if there is any hope of limiting global temperature rise.

In the face of all this, the new WRI study emphasises the positive potential of Chinese finance to support a global low carbon shift. It ends with some strong recommendations:

- The Chinese government should require financial institutions receiving Chinese government special funds to consider NDCs when developing their investment strategies. All the multilateral development banks, including the Asian Development Bank and the World Bank Group, have begun to formally incorporate reviews of NDCs into the development of their country strategies, and Chinese financial institutions could apply a similar practice.

- Governments of BRI countries should update their NDCs with sufficient granularity and quantitative information, national strategies, and associated project pipelines to financial institutions, including Chinese. This will help ensure that NDCs are used as potential points of focus for green BRI activities.

- A green BRI strategy will also need to consider how to address issues of equity and access to finance. Chinese investments in the BRI region have concentrated on the oil, gas, and petrochemical industries in a few BRI countries—mainly higher-middle-income and high-income countries. If BRI is to become a development initiative to improve connectivity and support sustainable development across many countries, more financial flows will be needed to support projects in lower-middle-income and low-income countries.

- Independent organisations should conduct research on drivers of financing decisions by different types of Chinese financial institutions and enterprises; and Chinese institutions should allow greater transparency on financial flows to the BRI countries.